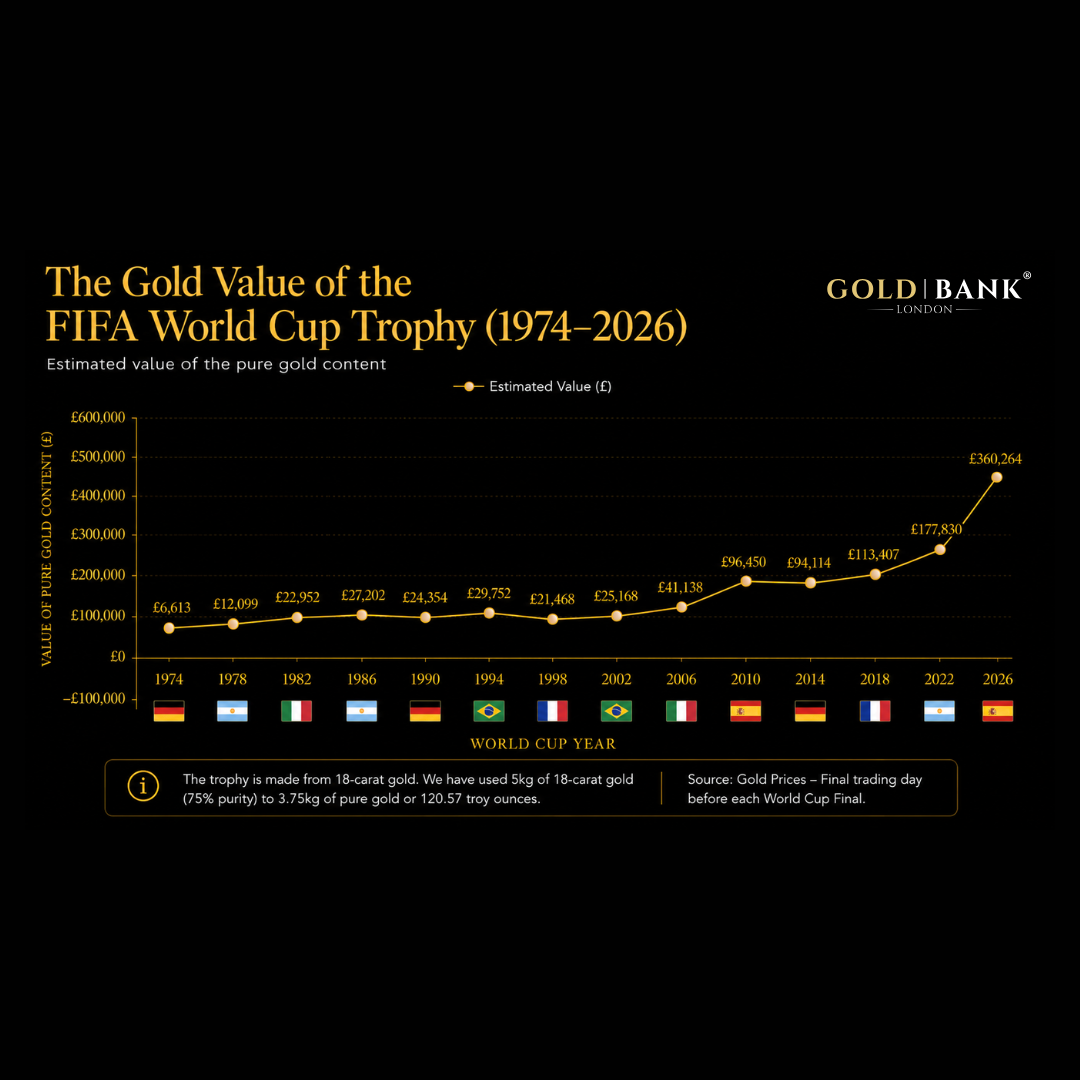

In Stock

In Stock

Low Stock

Low Stock

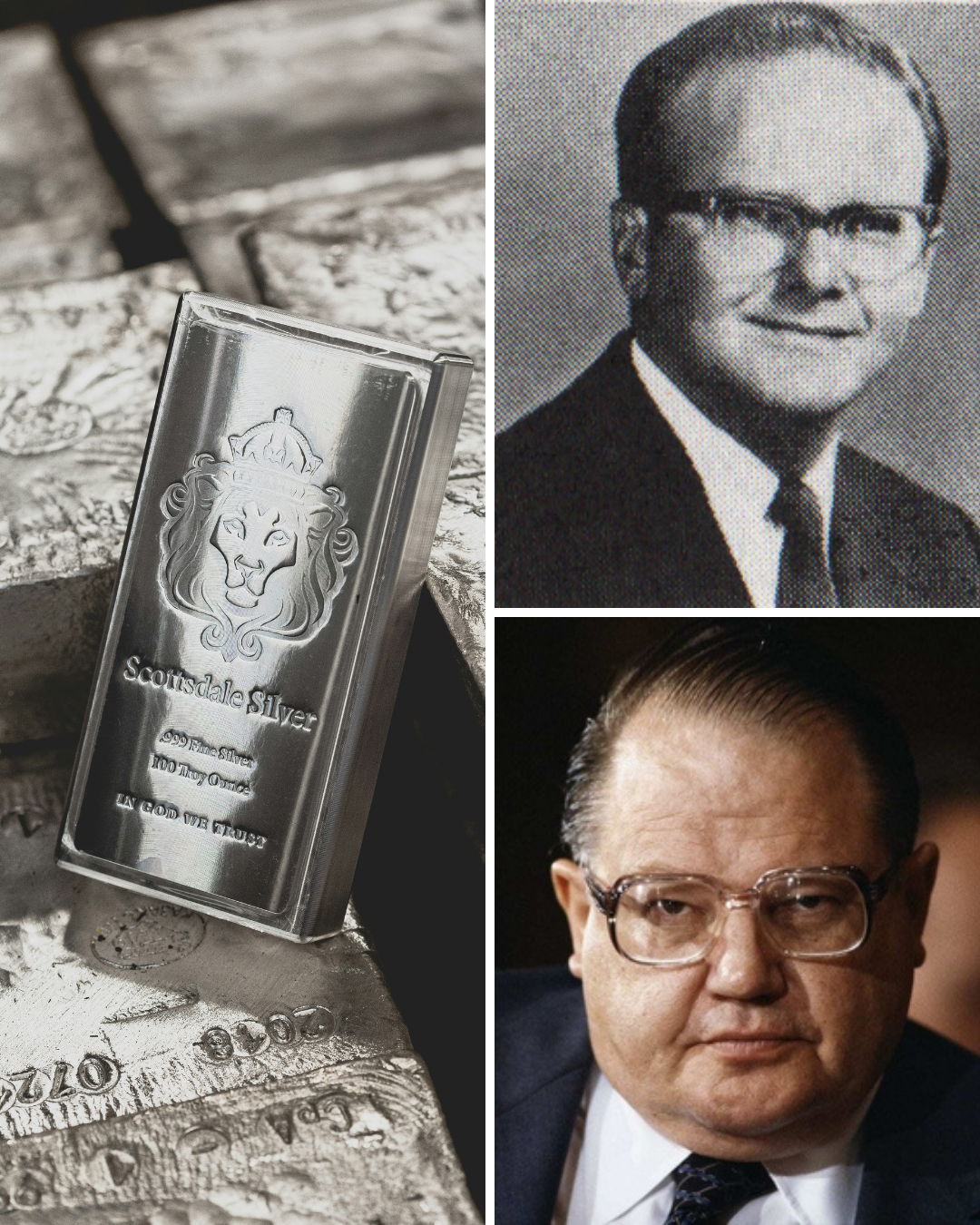

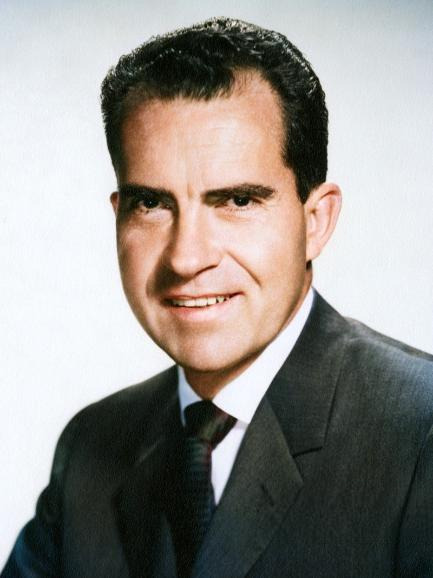

On 15 August 1971, the global financial system changed.

Then US President Richard Nixon went on television to announce that the United States would suspend the dollar’s convertibility into gold for foreign governments and central banks. It was presented as a temporary step to protect the US economy. In reality, it marked the beginning of the end for the gold-backed system which had supported global finance since the Second World War.

From then on, the world began moving towards currencies shaped by policy and market trust, and away from money tied to a physical asset. Inflation, interest rates and currency movements have behaved differently ever since.

More than fifty years later, that decision still shapes how the modern monetary system works and why physical gold continues to feature in many investors’ long-term thinking.

What was the gold standard?

The gold standard is a system whereby a country’s currency is directly linked to a fixed amount of gold. In practice, money could be exchanged for a set quantity of gold, which built trust and limited how much currency governments could create – because they couldn’t create unlimited amounts without the physical gold to back it .

Before 1971, much of the global monetary system was anchored to gold.

After the Second World War, the world moved into the Bretton Woods system. The Bretton Woods system was the post-war monetary framework agreed by 44 countries in 1944 which:

- Fixed the US dollar to gold at $35 per ounce

- Pegged major currencies to the US dollar

- Allowed foreign governments and central banks to exchange dollars for US gold

At the time, the United States held most of the world’s official gold reserves, which gave the system early credibility. The setup also cemented the dollar as the world’s reserve currency and put the US firmly at the centre of global finance.

Why was the Bretton Woods system agreed? Well the goal was first and foremost, stability. By fixing currencies to the dollar, exchange rates became far more predictable for governments, businesses and investors. Inflation was expected to stay under control.

For a while, the system worked well but as the global economy grew and more dollars flowed around the world, pressure on the gold link began to build.

The pressure building in the 1960s

The Bretton Woods framework relied on the fact that the United States could honour its promise to convert dollars into gold. But by the early 1960s, cracks in the system were starting to show. Confidence began to wobble as the global economy expanded and the number of dollars in circulation grew far faster than the amount of gold sitting in US vaults.

In addition to this, US government spending rose sharply during the 1960s, driven by the Vietnam War and major domestic programmes. At the same time, Europe and Japan were rebuilding after the war and becoming more competitive exporters. Dollars were flowing out of the United States and piling up overseas.

Foreign governments were holding more and more dollars, and while the US gold supply was growing only slowly, the gap between the two was becoming harder to ignore.

Some countries began testing the system by converting their dollar reserves into gold. Each conversion chipped away at US gold reserves. It raised the question: what would happen if too many countries asked for their gold at the same time? Fears of a run on US gold were very real.

Behind the scenes, policymakers tried a series of temporary fixes to steady the ship which bought them time, but did not solve the underlying problem.

By the end of the decade, confidence in the dollar’s gold link was under strain which set the stage was for the events of August 1971.

Why Nixon ended the gold standard in 1971

By the summer of 1971, US policymakers were running out of room to manoeuvre.

What had once been a manageable strain was now a live policy problem sitting right on the President’s desk.

Over a tense weekend at Camp David, Nixon and his economic team agreed to close the so-called gold window, preventing foreign governments and central banks from exchanging dollars for gold.

The announcement was part of a wider package of emergency measures all aimed at stabilising the US economy and relieving pressure on the dollar. These included a 90-day freeze on wages and prices and a temporary import surcharge.

Although presented as a temporary move, the gold window never reopened. The modern era of fiat money was underway.

How markets reacted after Nixon ended the gold standard

Global markets were forced to adjust quickly, however, there were attempts to steady the situation. The most notable was the Smithsonian Agreement in December 1971, where major economies agreed to realign their exchange rates against the US dollar and allow currencies to move within slightly wider bands.

The hope was that this would relieve pressure on the dollar and restore confidence in the fixed-rate system. But the core problem hadn’t been solved. And, by 1973, major economies had largely abandoned fixed exchange rates and moved to floating currencies. From that point on, exchange rates were set by market forces rather than by formal pegs.

How did gold react? Well, sharply.

Freed from its fixed $35 per ounce price, it began a dramatic climb during the 1970s. By January 1980, gold had briefly touched around $850 per ounce.

Inflation also became a defining feature of the decade. Without the discipline of the gold link, monetary policy had more flexibility, but that came with consequences. Many advanced economies experienced sustained inflation through the 1970s.

Lesser-known facts about the Nixon gold decision

A few details from August 1971 that often get overlooked:

- Nixon made the announcement on a Sunday evening, when markets were closed

- The timing limited the risk of immediate panic selling

- The move was publicly framed as protecting the dollar from international “speculators”

- The US gold window closed almost overnight, with little warning to trading partners

- Private gold ownership in the US had only recently been relegalised in 1974, after being restricted for decades

How the end of the gold standard affects today’s investors

More than fifty years on, the events of 1971 still shape how the financial world works.

Fiat money is currency which has value because governments declare it legal tender and people trust it, rather than because it is backed by a physical asset. When the link between the dollar and gold was broken, the global system moved fully into the era of fiat money. It gave central banks far more room to manage the economy, but it also removed the hard constraint which gold used to provide.

As a result, gold stopped being a fixed reference point inside the monetary system and became a freely traded asset with its own market price. From that point on, its own value has been driven by supply, demand and investor sentiment.

In the decades since, periods of economic uncertainty have repeatedly reminded investors of gold’s value; when confidence in currencies or financial markets comes under pressure, attention often turns back to assets that sit outside the policy-driven system.

Could the gold standard ever return?

From time to time, calls to revive the gold standard resurface. Advocates such as former US congressman Ron Paul and economist Judy Shelton have argued that tying money more closely to gold could impose greater monetary discipline. However, this remains a minority view. Most economists today believe a full return would be impractical given the size and complexity of the modern global economy.

This is because modern economies are far larger and more complex than they were in the Bretton Woods era. Global trade volumes are higher, financial markets move faster and governments rely heavily on the ability to adjust monetary policy during crises. Reintroducing a strict gold link would significantly reduce that flexibility.

There is also a practical question of scale. The amount of gold required to credibly back today’s global money supply would be enormous, and agreeing new fixed exchange rates across major economies would be politically challenging, to say the least.

This is the second article in our series exploring the major decisions that have shaped gold’s role in the modern financial system. If you would like to understand how gold could fit into your own long-term plans, you can explore more of our latest guides and tools.